Targeted Protein Degradation: Designed to destroy

Targeted protein degradation (TPD) has moved from a highly experimental concept to one of the most closely watched modalities in biopharma. What began with first-generation PROTACs (proteolysis-targeting chimeras) has evolved into a broader "induced proximity" field that now includes molecular glue degraders, degrader-antibody conjugates (DACs), lysosome-targeting chimeras (LYTACs), RNA degraders and other proximity-based therapeutics.

The sector is entering a decisive phase in 2026. Multiple late-stage clinical programmes are approaching potential regulatory milestones, big pharma companies are expanding partnerships, and investors increasingly view induced proximity technologies as a long-term platform rather than a niche drug discovery tool. Europe, meanwhile, has emerged as a strategically important – though still smaller – hub compared with the United States and China.

From PROTACs to proximity drugs

The core idea behind targeted protein degradation differs fundamentally from classical inhibition. Rather than blocking a protein’s active site, degraders recruit the cell’s own protein disposal machinery to eliminate the disease-driving protein entirely. This opens the possibility of targeting proteins previously considered “undruggable”, including transcription factors and scaffold proteins.

First-generation PROTACs use bifunctional molecules that connect a target protein to an E3 ubiquitin ligase, triggering proteasomal degradation. Molecular glues, by contrast, are typically smaller compounds that stabilise interactions between proteins and degradation machinery.

The broader “proximity drug” concept now extends beyond degradation toward induced stabilisation, trafficking and modulation of protein interactions.

Industry observers increasingly see the field evolving beyond classical PROTAC chemistry. Next-generation approaches now include alternative ligases, membrane-targeted degraders and non-proteolytic induced proximity mechanisms.

The US still leads the clinical race

The United States remains the dominant force in TPD, driven by venture funding, academic spinouts and deep pharma partnerships. Companies such as Arvinas, C4 Therapeutics, Kymera Therapeutics, Nurix Therapeutics and Monte Rosa Therapeutics remain among the best-funded and most clinically advanced players.

Arvinas is widely regarded as the sector pioneer and in fact delivered the first approved PROTAC therapeutic in spring this year for its oestrogen receptor degrader vepdegestrant, partnered with Pfizer (see special section next page).

Kymera Therapeutics has broadened the modality into immunology and inflammation, particularly with STAT6-targeting programmes. Nurix Therapeutics has focused heavily on oncology and degrader-antibody conjugates, while C4 Therapeutics continues expanding its long-standing relationship with Roche.

The Roche–C4 collaboration announced in April 2026 highlights how quickly the field is converging with ADC technology. The companies are jointly developing degrader-antibody conjugates designed to combine the targeting specificity of antibodies with catalytic protein degradation. The deal includes $20m upfront and more than $1bn in milestones.

At the same time, Gilead Sciences recently exercised its option on Kymera’s CDK2 degrader KT-200, reinforcing the view that large pharma companies increasingly consider degraders part of mainstream oncology strategy rather than experimental science.

Europe: Strong science, smaller capital pools

Europe’s degrader ecosystem is scientifically competitive but structurally different. Compared with the US, European companies generally operate with smaller financing rounds and rely more heavily on strategic pharma alliances.

Switzerland has become Europe’s most important TPD centre thanks to the presence of Novartis and Roche. Novartis has aggressively expanded into molecular glue degraders and proximity chemistry through multiple licensing deals.

One of the most significant recent transactions came in late 2024, when Novartis agreed to pay Monte Rosa Therapeutics $150m upfront in a deal potentially worth more than $2bn. The agreement centred on MRT-6160 and broader molecular glue programmes.

Novartis had already strengthened its position through a separate agreement with Arvinas around the androgen receptor degrader ARV-766 in prostate cancer.

In Europe, especially Georg Winter´s Lab (Vienna, Austria) is an incubator for degraders, leading to the foundation of C4 Therapeutics and Proxygen, who kick started with a pre-foundational cooperation with Boehringer Ingelheim.

Germany has also become increasingly active, particularly around Frankfurt/M, Munich and Heidelberg, where academic groups are working on novel ligases, cereblon biology and next-generation proximity chemistry.

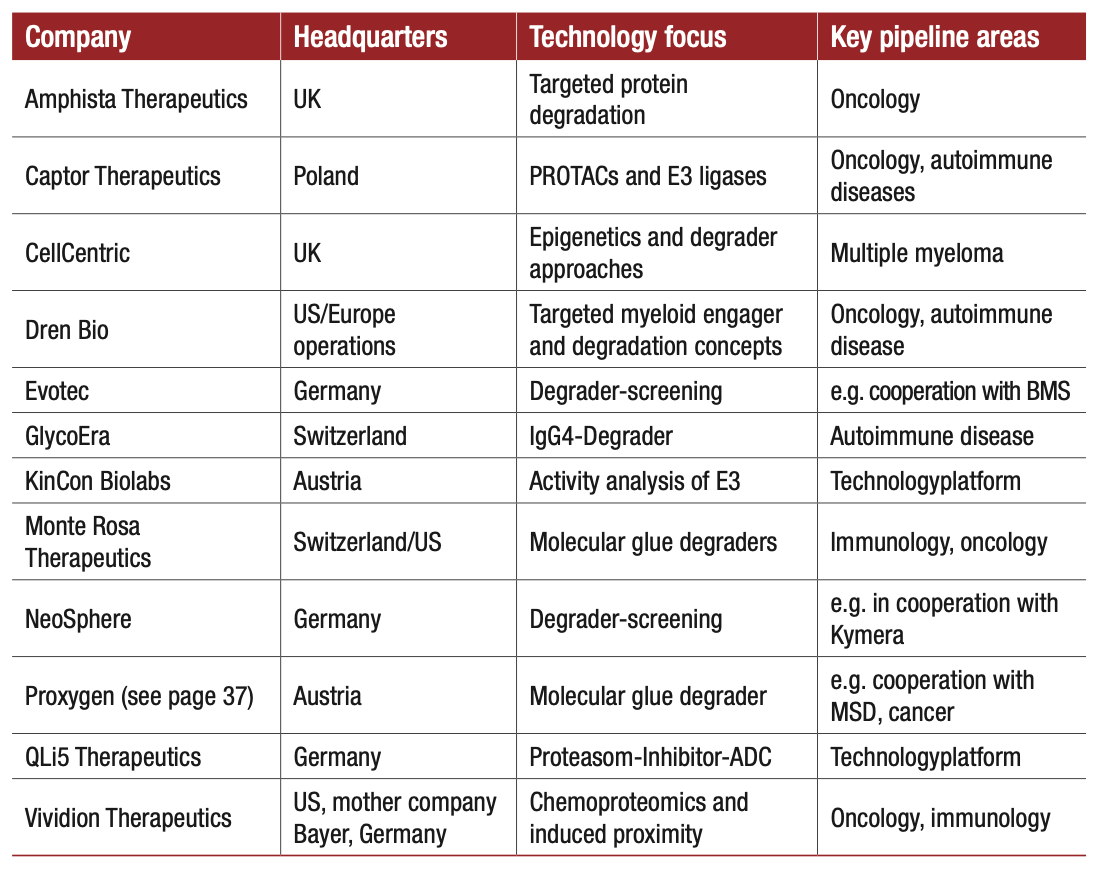

A selection of European biotech companies active in the field is shown in the table. However, Europe still lacks the dense concentration of listed TPD companies seen in Boston or San Diego – and in China.

A selection of European biotech companies active in the field of targeted protein degradation.

China accelerates rapidly

China has emerged as the fastest-growing geography in the degrader field. Chinese biotech companies initially focused on licensing Western degrader technology, but domestic platforms are now becoming increasingly sophisticated.

Companies such as Cullgen, Hinova Pharmaceuticals and Brii Biosciences have built internal degradation platforms, while larger Chinese pharmas are entering the space through partnerships and licensing. Several Chinese AR degraders and molecular glue programmes are now competing directly with Western assets in prostate cancer and haematology.

China’s advantages include rapid medicinal chemistry optimisation, lower development costs and growing expertise in translational oncology.

Beyond oncology

Oncology still dominates the TPD landscape, but the field is rapidly diversifying into immunology, neuroscience and fibrosis.

STAT6 degradation has become one of the sector’s most closely watched immunology approaches, particularly after encouraging early signals from Kymera. Molecular glues are also being explored for autoimmune diseases and neurodegeneration.

At the same time, companies are moving beyond conventional proteasome targeting. New approaches aim to degrade extracellular proteins, membrane proteins and RNA-associated complexes that classical PROTACs struggle to address. This diversification is critical because first-generation clinical data in oncology have been mixed. Some early PROTACs showed pharmacokinetic limitations due to molecular size and complexity. Community discussions among biotech investors and scientists increasingly suggest that the real long-term value may lie in previously inaccessible targets – drugging the undruggable.

Intense M&A and deal activity

The sector’s commercial momentum is increasingly visible in partnership activity. Over the past two years, nearly every major pharma company has entered some form of degrader collaboration.

Key recent deals include:

- Roche and C4 Therapeutics expanding their DAC collaboration in 2026.

- Novartis licensing Monte Rosa’s molecular glue portfolio.

- Gilead Sciences opting into Kymera’s CDK2 degrader programme.

- Multiple ADC and DAC convergence deals signalling that degraders may increasingly become payloads in targeted delivery systems.

The convergence of ADCs and degraders is particularly important. Several pharma companies now view DACs as a possible next-generation successor to traditional ADC payloads because degraders could potentially avoid resistance mechanisms and broaden therapeutic windows.

The regulatory path may initially resemble the evolution of ADCs: early approvals in oncology followed by expansion into broader therapeutic areas once chemistry, delivery and safety improve. At the same time, the field is moving beyond classical bifunctional PROTACs towards alternative mechanisms such as intramolecular bivalent glues (IBGs), indirect degraders and so-called “degradation tails”. These approaches exploit natural protein interactions or induce conformational changes that activate the cell’s endogenous degradation machinery.

Targeted instability and ternary complex formation, which enable individual members of large protein families to be degraded with remarkable precision, are emerging as promising new approaches and are further expanding the growing array of therapeutic modalities with a common goal: to attract investors.